8주차: 5월 25일 ~ 5월 29일

멀티캠퍼스 부트캠프 8주차 요약✍️

[ 5/25 ] 대체공휴일 휴강

[ 5/26 ] 딥러닝: RNN, LSTM_회귀

[ 5/27 ] 딥러닝: LSTM_분류

[ 5/28 ] 투자 전략: Bollinger Band, BuyandHold

[ 5/29 ] 투자 전략: Momentum

5월 26일👩🏻💻

오늘의 소감: 틀리면서 배우는 딥~러~닝~

학습률 0.001을 0.01로 바꾸니까 MSE 진짜 난리나던데 하...🫠

0 하나를 못봐서 점심시간 내내 코드를 보고 있었다.

💻 RNN

AAPL(애플 주식) 데이터 활용

라이브러리, 데이터 로드

import pandas as pd

import matplotlib.pyplot as plt

import torch

import torch.nn as nn

import torch.optim as optim

from torch.utils.data import Dataset, DataLoader

from sklearn.preprocessing import StandardScaler, MinMaxScaler

from sklearn.metrics import mean_squared_error, r2_score

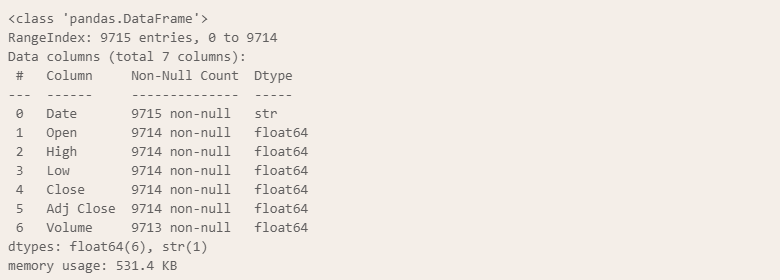

df = pd.read_csv("../csv/aapl.csv")

df.info()

데이터 전처리

df.dropna(inplace=True)

df = df[['Date', 'Adj Close']]

values = df[['Adj Close']].values

df['Adj Close'].values.reshape(-1, 1)

split_idx = int(len(values) * 0.75)

train_data = values[:split_idx]

test_data = values[split_idx:]

# MinMaxScaler로 데이터 정규화

scaler = MinMaxScaler()

train_sc = scaler.fit_transform(train_data)

test_sc = scaler.transform(test_data)

# 스케일링이 완료된 데이터를 Tensor로 변환

train_sc = torch.tensor(train_sc, dtype=torch.float32)

test_sc = torch.tensor(test_sc, dtype=torch.float32)Dataset 생성, DataLoader 사용을 통한 train_dl/test_dl 생성

class WindowDataset(Dataset):

def __init__(self, _data, _window):

# _data : tensor, array 1차원 데이터 형태

# _window : 구간의 크기

self.data = _data

self.window = _window

# DataLoader에서 사용 가능한 인덱스의 최대 값

self.n = len(_data) - _window

def __len__(self):

return self.n

def __getitem__(self, idx):

# idx : 0 ~ self.n-1 사이의 정수가 대입 (DataLoader에서 자동으로 대입)

x = self.data[idx:idx + self.window]

y = self.data[idx + self.window]

return x, y

# WindowDataset에 데이터를 대입

train_ds = WindowDataset(train_sc, _window=60)

test_ds = WindowDataset(test_sc, _window=60)

# Dataset를 DataLoader로 생성

train_dl = DataLoader(train_ds, batch_size=128, shuffle = True, drop_last = True)

test_dl = DataLoader(test_ds, batch_size=256, shuffle=False, drop_last = False)RNN Model, 검증 데이터 평가 함수 생성

RNN Model

# RNN 모델 정의

class RNNModel(nn.Module):

def __init__(self,

input_size,

hidden_size = 64,

num_layers = 1,

dropout = 0.0,

nonlinearity = 'tanh',

bidirectional = False):

super(RNNModel, self).__init__()

# super().__init__()

self.rnn = nn.RNN(

input_size = input_size,

hidden_size = hidden_size,

num_layers = num_layers,

dropout = dropout,

nonlinearity = nonlinearity,

bidirectional = bidirectional,

# batch_first가 False인 경우, 입력 데이터(구간의 개수, 배치크기, 입력 데이터 피쳐의 수)

# (배치 크기, 구간의 크기, 입력 피쳐의 개수) --> True로 변경

batch_first = True

)

# output_feature가 역방향을 포함한다면 2배로 늘어난다.

if bidirectional:

hidden_size *= 2

print(f"hidden_size : {hidden_size}")

self.model = nn.Linear(hidden_size, 1)

def forward(self, x):

out, h_n = self.rnn(x)

last_hidden = h_n[-1]

result = self.model(last_hidden)

return result# 모델 학습 시 검증 데이터를 이용하여 모델의 성능을 평가 할수 있도록 검증 데이터 평가 함수

@torch.no_grad()

def evaluate_mse(dataloader, model):

# dataloader -> 검증 데이터셋의 dataloader

model.eval()

total_loss = 0

total_n = 0

for x, y in dataloader:

x = x.float()

y = y.float()

pred = model(x)

loss = nn.MSELoss()(pred, y)

total_loss += loss.item() * x.size(0)

total_n += x.size(0)

return total_loss / max(total_n, 1)RNN Model 호출, 평가 지표, optimizer 생성

aapl_model = RNNModel(

input_size = 1,

hidden_size = 128

)

criterion = nn.MSELoss()

optimizer = optim.Adam(aapl_model.parameters(), lr = 0.001) # 문제의 0.01과 0.001...train_history, test_history = [], []

for epoch in range(20):

aapl_model.train()

running, n_seen = 0.0, 0

for x, y in train_dl:

x = x.float()

y = y.float()

pred = aapl_model(x)

loss = criterion(pred, y)

optimizer.zero_grad()

loss.backward()

# 가중치 발산 방지

nn.utils.clip_grad_norm_(aapl_model.parameters(), 1.0)

optimizer.step()

running += loss.item() * y.size(0)

n_seen += y.size(0)

train_mse = running / n_seen

test_mse = evaluate_mse(test_dl, aapl_model)

train_history.append(train_mse)

test_history.append(test_mse)

print(f"Epoch {epoch+1} Train MSE: {round(train_mse, 8)} Test MSE: {round(test_mse, 8)}")

시각화

aapl_model.eval() # 평가 모드

preds = []

trues = []

with torch.no_grad():

for x, y in test_dl:

x = x.float()

y = y.float()

pred = aapl_model(x)

preds.append(pred.cpu())

trues.append(y.cpu())

# cat 함수: pd.concat() 과 같은 역할

preds = torch.cat(preds, dim=0).squeeze(-1).numpy()

trues = torch.cat(trues, dim=0).squeeze(-1).numpy()

# 시각화

plt.figure(figsize = (14, 10))

plt.plot(preds[:600], label = 'Preds')

plt.plot(trues[:600], label = 'Trues')

plt.legend()

plt.grid()

plt.show()

💻 LSTM

AAPL 데이터 활용

코드는 RNN과 매우 유사하지만, 예측값을 2개 돌려주는 RNN과 달리 LSTM은 3개를 돌려준다.

또한 nn.LSTM에는 nn.RNN에 없는 head_type이라는 인자가 존재한다.

라이브러리

import pandas as pd

import matplotlib.pyplot as plt

import torch

import torch.nn as nn

import torch.optim as optim

from torch.utils.data import Dataset, DataLoader

from sklearn.preprocessing import MinMaxScaler

from sklearn.model_selection import train_test_split함수화를 위한 작업

# 하나의 함수화

# 매개변수로 사용할 데이터들은 어떤 것이 있을까?

# 파일의 경로를 지정하는 변수 (read_csv)

file_path = '../csv/aapl.csv'

# 구간(window) 설정 (Dataset)

window = 60

# batch size 지정 (DataLoader)

x_batch = 64

y_batch = 256

# 기여도 (optimizer)

lr = 0.001

# 반복 학습 횟수

epochs = 20

# 은닉층에서의 뉴런(feature)의 개수

hidden_cnt = 64

# Layer 설정값

layer_cnt = 1

# train, test 비율

train_ratio = 0.8

# 은닉층, 셀 구조에서 어떤 부분을 사용할 것인가?

# 'h': 은닉층 사용 // 'c': 셀 사용 // 'h_c': 둘 다 사용

head_type = 'h_c'데이터 로드, 전처리

df = pd.read_csv(file_path)

df.dropna(inplace=True)

df['Date'] = pd.to_datetime(df['Date'])

X = df[['Adj Close', 'Volume']].astype(float).values

y = df[['Adj Close']].astype(float).values

X_train, X_test, y_train, y_test = train_test_split(

X, y, train_size = train_ratio, shuffle = False

)

scaler_x = MinMaxScaler()

scaler_y = MinMaxScaler()

X_train_sc = scaler_x.fit_transform(X_train)

X_test_sc = scaler_x.transform(X_test)

y_train_sc = scaler_y.fit_transform(y_train)

y_test_sc = scaler_y.transform(y_test)Dataset 생성, DataLoader 사용을 통한 train_dl/test_dl 생성

class WindowDataset(Dataset):

def __init__(self, _x, _y, _window):

self.x = _x

self.y = _y

self.window = _window

self.n = (len(_x) - _window)

def __len__(self):

return max(self.n, 1)

def __getitem__(self, idx):

x = self.x[idx : idx + self.window]

y = self.y[idx + self.window]

x_tensor = torch.tensor(x, dtype = torch.float32)

y_tensor = torch.tensor(y, dtype = torch.float32)

return x_tensor, y_tensor

train_ds = WindowDataset(X_train_sc, y_train_sc, window)

test_ds = WindowDataset(X_test_sc, y_test_sc, window)

train_dl = DataLoader(train_ds, shuffle = True, drop_last = True, batch_size = x_batch)

test_dl = DataLoader(test_ds, shuffle = False, drop_last=False, batch_size = y_batch)LSTM 정의

class LSTMModel(nn.Module):

def __init__(

self,

input_size,

hidden_size = 64,

num_layers = 1,

dropout = 0.0,

bidirectional = False,

batch_first = True,

head_type = 'h'

):

super(LSTMModel, self).__init__()

# LSTM 기본 설정

self.lstm = nn.LSTM(

input_size = input_size,

hidden_size = hidden_size,

num_layers = num_layers,

dropout = dropout,

bidirectional = bidirectional,

batch_first = batch_first

)

# bidirectional이 True면 out feature의 개수가 2배

hidden_size = hidden_size * (2 if bidirectional else 1)

# head_type에 따라서 출력의 feature 개수가 달라진다.

if head_type in ['h', 'c']:

#if (head_type == 'h') | (head_type == 'c')

pass

elif head_type == 'h_c':

hidden_size = hidden_size * 2

else:

print('head_type의 인자값을 잘못 입력하였습니다. ("h", "c", "h_c")를 사용해주세요')

# 선형 모델 생성

self.model = nn.Linear(hidden_size, 1)

# 객체 안에 독립적인 데이터를 저장

self.head_type = head_type

# 순전파 함수 정의

def forward(self, x):

# 순전파의 예측값 (RNN은 2개를 되돌려줌, LSTM은 3개를 되돌려줌)

out, (h_n, c_n) = self.lstm(x)

# 은닉층의 가장 마지막값 저장

h_last = h_n[-1]

c_last = c_n[-1]

if self.head_type == 'h':

feat = h_last

elif self.head_type == 'c':

feat = c_last

elif self.head_type == 'h_c':

feat = torch.cat([h_last, c_last], dim = -1)

return self.model(feat)여기서 __init__ 함수에 들어간 parameter들은 기본값으로 사용될 것이다.

모델 생성

model = LSTMModel(input_size = 2, hidden_size = hidden_cnt, head_type = head_type)

model

손실 함수, 옵티마이저 정의

criterion = nn.MSELoss()

optimizer = optim.Adam(model.parameters(), lr = lr)평가 함수 생성

# 검증 데이터의 loss값 확인하는 함수

# @torch.no_grad()

def evaluate_mse(dl):

model.eval()

total_loss, total_n = 0.0, 0

# 데코레이터 또는 여기 사용

with torch.no_grad():

for x, y in dl:

x = x.float()

y = y.float()

pred = model(x)

loss = criterion(pred, y)

total_loss += loss.item() * y.size(0)

total_n += y.size(0)

return total_loss / max(total_n, 1)반복 학습

# 반복 학습

test_history = []

for epoch in range(epochs):

model.train()

total_loss, total_n = 0.0, 0

for x, y in train_dl:

x = x.float()

y = y.float()

pred = model(x)

loss = criterion(pred, y)

optimizer.zero_grad()

loss.backward()

# 기울기 발산 방지 (이 자리 아니면 소용 없음)

nn.utils.clip_grad_norm_(model.parameters(), 1.0)

optimizer.step()

total_loss += loss.item() * y.size(0)

total_n += y.size(0)

train_loss = total_loss / max(total_n, 1)

test_loss = evaluate_mse(test_dl)

test_history.append(test_loss)

print(f"Epoch: {epoch+1}, train_mse: {round(train_loss, 4)}, test_mse: {round(test_loss, 4)}")

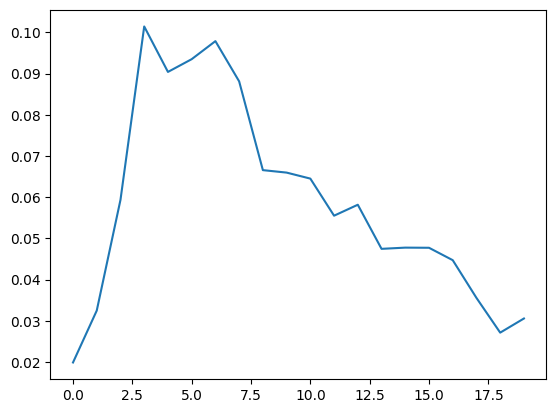

간단 시각화

# test_history를 그래프로 시각화

plt.plot(test_history)

plt.show()

예측값 생성

model.eval()

preds, trues = [], []

with torch.no_grad():

for x, y in test_dl:

x = x.float()

pred = model(x)

preds.append(pred)

trues.append(y)

# tensor 데이터들을 하나로 합쳐주고 차원을 벗겨낸 다음 array로 변환

preds = torch.cat(preds, dim=0).numpy()

trues = torch.cat(trues, dim=0).numpy()

# 스케일링 데이터를 원본 데이터로 변환

pred_origin = scaler_y.inverse_transform(preds).squeeze(-1)

true_origin = scaler_y.inverse_transform(trues).squeeze(-1)시각화

plt.figure(figsize = (16, 10))

plt.plot(pred_origin, label = 'Pred Origin')

plt.plot(true_origin, label = 'True Origin')

plt.legend()

plt.grid()

plt.xlabel('Date')

plt.ylabel('Adj Close')

plt.show()

5월 27일👩🏻💻

오늘의 소감: 시간이 순식간에 흘러간다... 분명 한 건 많지 않은 것 같은데 뇌에 과부하가 걸려서 진행을 못 하는 느낌🫠

💻 LSTM_분류

날씨 데이터 활용

라이브러리, 데이터 로드

import pandas as pd

import numpy as np

import requests

import torch

import torch.nn as nn

import torch.optim as optim

import matplotlib.pyplot as plt

import platform

from sklearn.metrics import accuracy_score

from torch.utils.data import Dataset, DataLoader

from sklearn.preprocessing import MinMaxScaler

---

url = "https://archive-api.open-meteo.com/v1/archive"

params = {

'latitude': 37.5665,

'longitude': 126.9780,

'start_date': '2025-01-01',

'end_date': '2025-12-31',

'hourly': 'temperature_2m,relative_humidity_2m,surface_pressure,wind_speed_10m,rain'

}

res = requests.get(url, params = params)

data = res.json()

# 날씨 데이터들을 따로 추출

df = pd.DataFrame(data['hourly'])

df.columns = ['측정 시간', '기온', '상대 습도', '지면 기압', '풍속', '강수량']데이터 전처리

x = df[['기온', '상대 습도', '지면 기압', '풍속']].values

y = df['target'].values

x_sc = MinMaxScaler().fit_transform(x)Dataset 생성, DataLoader 사용 train_dl/test_dl 생성

class windowDS(Dataset):

def __init__(self, _x, _y, _window):

self.x = _x

self.y = _y

self.window = _window

self.n = len(_x) - _window

def __len__(self):

return self.n

def __getitem__(self, idx):

x = self.x[ idx : idx + self.window ]

y = self.y[ idx + self.window ]

x_tensor = torch.tensor(x).float()

y_tensor = torch.tensor(y).long()

return x_tensor, y_tensor

window = 72

train_ds = windowDS(x_sc, y, window)

train_dl = DataLoader(train_ds, batch_size = 64, shuffle=False)LSTM 모델 생성

class LSTMclf(nn.Module):

def __init__(

self,

input_size,

hidden_size

):

super(LSTMclf, self).__init__()

self.lstm = nn.LSTM(

input_size = input_size,

hidden_size = hidden_size,

batch_first = True

)

self.model = nn.Linear(hidden_size, 2)

def forward(self, x):

out, (h_n, c_n) = self.lstm(x)

# h_n[-1], c_n[-1]: bidirectional이 False인 경우 사용 가능

# True인 경우 역방향의 아웃풋 피쳐만 불러온다.

# out: 3차원 데이터셋 → [batch, window, feature]

# 2차원 데이터셋의 형태로 변경 → out[:, -1, :] → [batch, feature]

pred = self.model(out[:, -1, :])

return pred모델 정의, 손실 함수, 옵티마이저 생성

model = LSTMclf(input_size = x.shape[1], hidden_size=32)

criterion = nn.CrossEntropyLoss()

optimizer = optim.Adam(model.parameters(), lr=0.001)반복 학습

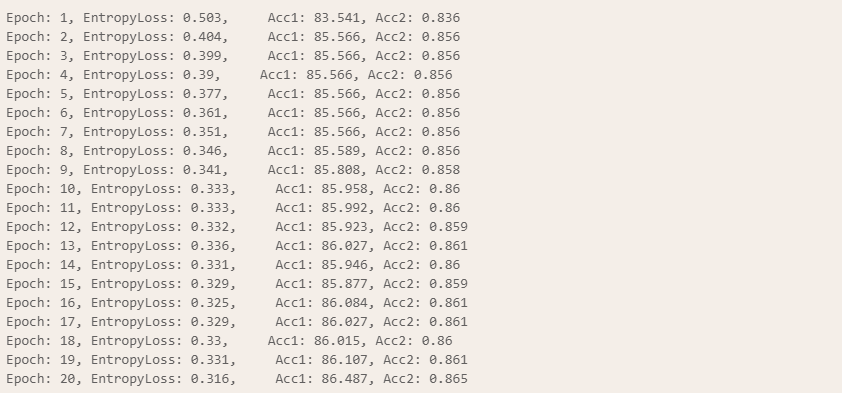

model.train()

for epoch in range(20):

total_loss, total_n = 0.0, 0

current1 = current2 = 0

acc_list = []

for x, y in train_dl:

res = model(x)

loss = criterion(res, y)

optimizer.zero_grad()

loss.backward()

nn.utils.clip_grad_norm_(model.parameters(), 1.0)

optimizer.step()

total_loss += loss.item()

total_n += y.size(0)

_, pred = torch.max(res, 1)

acc = accuracy_score(y.numpy(), pred.numpy())

acc_list.append(acc)

current1 += (y == pred).sum().item()

train_loss = total_loss / len(train_dl)

mean_current = (current1 / max(total_n, 1)) * 100

current2 = np.mean(acc_list)

print(f'Epoch: {epoch+1}, EntropyLoss: {round(train_loss, 3)}, \

Acc1: {round(mean_current, 3)}, Acc2: {round(current2, 3)}')

예측

model.eval()

eval_loader = DataLoader(train_ds, batch_size = 1000, shuffle=False)

# 첫번째 데이터만 로드

x, y = next(iter(eval_loader))

with torch.no_grad():

test_out = model(x)

_, test_pred = torch.max(test_out, 1)시각화

# 한글 인코딩을 위해

if platform.system() == 'Windows':

plt.rc('font', family = 'Malgun Gothic')

plt.rcParams['axes.unicode_minus'] = False

# 시각화

plt.figure(figsize=(15, 5))

plt.plot(y.numpy(), label = '실제 강수 여부', color = 'gray', drawstyle = 'steps-mid', alpha = 0.5)

plt.plot(test_pred.numpy(), label = 'LSTM의 결과', color = 'blue', linestyle = '--', drawstyle = 'steps-mid', alpha=0.7)

plt.yticks([0, 1], ['맑음(0)', '비(1)'])

plt.legend()

plt.show()

5월 28일👩🏻💻

오늘의 소감: 클래스 지옥😵

💻 Bollllinger Band

Amazon 주식 데이터(AMZN) 활용

라이브러리, 데이터 로드

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from datetime import datetime

df = pd.read_csv('../csv/AMZN.csv', index_col = 'Date')

df.head()

데이터 전처리, 파생 변수 생성

flag = df.isin( [np.nan, np.inf, -np.inf] ).any(axis = 1)

df = df.loc[~flag, ]

# 종가 이외의 데이터를 제외

df = df[['Adj Close']]

# 이동평균선 → rolling

df['center'] = df['Adj Close'].rolling(20).mean()

# 상단 밴드, 하단 밴드 생성

std_value = 2 * df['Adj Close'].rolling(20).std()

df['ub'] = df['center'] + std_value

df['lb'] = df['center'] - std_value

# index 값을 시계열로 변경

df.index = pd.to_datetime(df.index)

# 투자 시작 시간 설정

start = '2010-01-01'

test_df = df.loc[start: , ]

test_df.head()보유 내역 추가

# 구매 상태를 입력할 수 있는 공간 생성

test_df['trade'] = ''

test_df.head()

상단 밴드보다 수정 주가가 높거나 같은 경우인데 현재 보유 중: 매도

상단 밴드보다 수정 주가가 높거나 같은 경우인데 보유 중 아님: 유지

하단 밴드보다 수정 주가가 낮거나 같은 경우인데 현재 보유 중: 유지

하단 밴드보다 수정 주가가 낮거나 같은 경우인데 보유 중 아님: 매수

수정 주가가 밴드 사이에 존재하는 경우인데 현재 보유 중: 유지

수정 주가가 밴드 사이에 존재하는 경우인데 보유 중 아님: 유지

for i in test_df.index:

# 상단 밴드보다 수정 종가가 높은 경우

if test_df.loc[i, 'Adj Close'] >= test_df.loc[i, 'ub']:

# 보유 중이라면 trade = '', 아니라면 trade = ''

test_df.loc[i, 'trade'] = ''

# 하단 밴드보다 수정 종가가 낮은 경우

elif test_df.loc[i, 'Adj Close'] <= test_df.loc[i, 'lb']:

# 보유 중이라면 trade = 'buy', 아니라면 trade = 'buy'

test_df.loc[i, 'trade'] = 'buy'

else:

# 보유 중인 경우 trade = 'buy', 보유 중이 아니면 trade = ''

# 전날의 trade가 buy인 경우: 보유 중

if test_df.shift().loc[i, 'trade'] == 'buy':

test_df.loc[i, 'trade'] = 'buy'

else:

test_df.loc[i, 'trade'] = ''수익률 계산

# 수익률 column 생성, 1로 채워준다

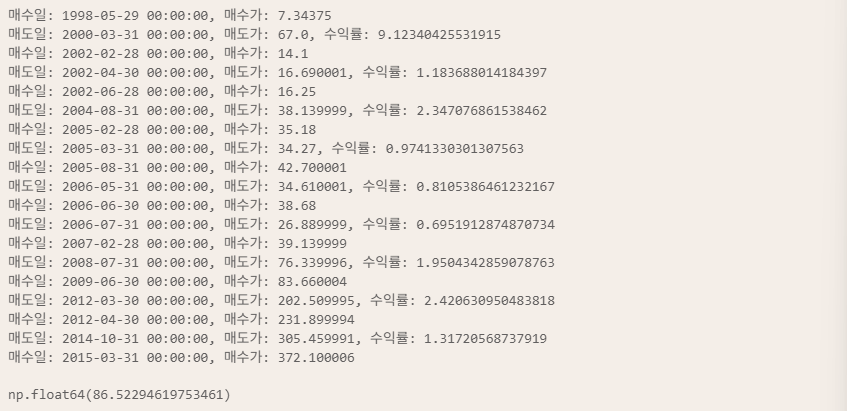

test_df['rtn'] = 1.0for i in test_df.index:

# 매수 가격 형성

if (test_df.shift().loc[i, 'trade'] == '') & (test_df.loc[i, 'trade'] == 'buy'):

buy = test_df.loc[i, 'Adj Close']

print(f'매수일: {i}, 매수가: {buy}')

# 매도 가격 형성

elif (test_df.shift().loc[i, 'trade'] == 'buy') & (test_df.loc[i, 'trade'] == ''):

sell = test_df.loc[i, 'Adj Close']

# 수익률 계산

rtn = sell / buy

test_df.loc[i, 'rtn'] = rtn

print(f'매도일: {i}, 매도가: {sell}, 수익률: {rtn}')

누적 수익률 계산 → rtn 누적곱

acc_rtn = 1.0

for i in test_df.index:

rtn = test_df.loc[i, 'rtn']

acc_rtn *= rtn

test_df['acc_rtn'] = test_df['rtn'].cumprod()

test_df.iloc[-1, -1]

# np.float64(3.138061358619031)번외: Buy and Hold

계산이 간단해서 제목을 따로 사용하진 않은 Buy and Hold...

# 투자 기간 첫날 → 매수가

# 투자 마지막 날 → 매도가

bnh_rtn = test_df.iloc[-1, 0] / test_df.iloc[0, 0]

print(bnh_rtn)

# 14.249095911087196💻 함수화

지금까지 만든 것들을 매개변수를 통일하여 하나의 클래스 속 3개의 함수로 연결짓는 과정

def create_band(

_df,

_col = 'Adj Close',

_start = '2010-01-01',

_end = datetime.now(),

_cnt = 20

):

df = _df.copy()

if 'Date' in df.columns:

df.set_index('Date', inplace=True)

df.index = pd.to_datetime(df.index)

df.index = df.index.tz_localize(None)

flag = df.isin( [ np.nan, np.inf, -np.inf ] ).any(axis=1)

df = df.loc[~flag, ]

df = df[[_col]]

df['center'] = df[_col].rolling(_cnt).mean()

std_value = 2 * df[_col].rolling(_cnt).std()

df['ub'] = df['center'] + std_value

df['lb'] = df['center'] - std_value

df = df.loc[_start:_end, ]

return dfdf2 = pd.read_csv('../csv/aapl.csv')

band_df = create_band2(df2)2. 보유 내역 생성 함수

def create_trade(_df):

# 기준 컬럼 이름을 어떻게 알 것인가?: 첫번째 함수의 return으로 나온 df의 첫번째 컬럼만

col = _df.columns[0]

df = _df.copy()

df['trade'] = ''

for i in df.index:

if df.loc[i, col] >= df.loc[i, 'ub']:

# 매도

df.loc[i, 'trade'] = ''

elif df.loc[i, col] <= df.loc[i, 'lb']:

# 매수

df.loc[i, 'trade'] = 'buy'

else:

if df.shift().loc[i, 'trade'] == 'buy':

df.loc[i, 'trade'] = 'buy'

else:

df.loc[i, 'trade'] = ''

return dftrade_df = create_trade(band_df)3. 수익률 계산 함수

def create_rtn(_df):

col = _df.columns[0]

df = _df.copy()

df['rtn'] = 1.0

# 수익률 계산

for i in df.index:

# 매수

if (df.shift().loc[i, 'trade'] == '') & (df.loc[i, 'trade'] == 'buy'):

buy = df.loc[i, col]

print(f"매수일: {i}, 매수가: {buy}")

print()

elif (df.shift().loc[i, 'trade'] == 'buy') & (df.loc[i, 'trade'] == ''):

sell = df.loc[i, col]

rtn = sell / buy

df.loc[i, 'rtn'] = rtn

print(f"매도일: {i}, 매도가: {sell}, 수익률: {rtn}")

print()

# 누적 수익률

df['acc_rtn'] = df['rtn'].cumprod()

# 최종 수익률

acc_rtn = df.iloc[-1, -1]

return df, acc_rtnrtn_df, acc_rtn = create_rtn(trade_df)

acc_rtn # np.float64(1.3923287814461949)

rtn_df

Class로 묶기

class Investing():

def __init__(self, _df, _col = 'Adj Close', _start = '2010-01-01', _end = datetime.now()):

self.df = _df

self.col = _col

self.start = _start

self.end = _end

# 바이앤홀드 함수

def bnh(self):

df = self.df.copy()

if 'Date' in df.columns:

df.set_index('Date', inplace=True)

df.index = pd.to_datetime(df.index)

df = df.loc[self.start:self.end, [self.col]]

buy = df.iloc[0, 0]

sell = df.iloc[-1, 0]

return sell / buy

# 볼린져 밴드 함수

def boll(self, _cnt = 20):

band_df = create_band(self.df, self.col, self.start, self.end, _cnt)

trade_df = create_trade(band_df)

rtn_df, acc_rtn = create_rtn(trade_df)

return rtn_df, acc_rtn간이 테스트

df3 = pd.read_csv('../csv/MSFT.csv')

invest = Investing(df3)

invest.bnh() # np.float64(5.6387313298309785)5월 29일👩🏻💻

오늘의 소감: 그래도 딥러닝을 하다가 pandas 활용하니까 살겠다...🥹

💻 Momentum

(전 월의 수정 주가/전 년도의 수정 주가) - 1로 구매 타이밍을 잡는 투자 전략

라이브러리, 데이터 로드

import pandas as pd

import numpy as np

from datetime import datetime

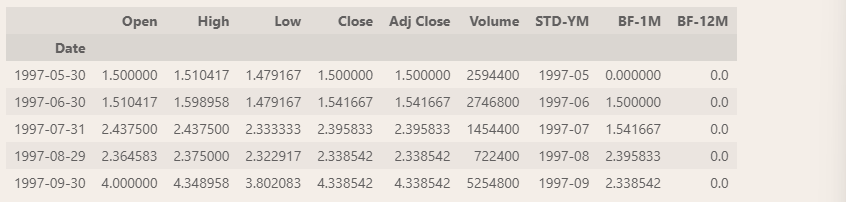

df = pd.read_csv('../csv/AMZN.csv', index_col='Date')

df.head()

데이터 전처리

# index 시계열로 변환

df.index = pd.to_datetime(df.index)

# index 데이터에서 년-월을 추출하여 STD-YM에 대입

df['STD-YM'] = df.index.strftime('%Y-%m')

# 월말만 모아놓은 데이터

month_last_df = df.groupby('STD-YM').tail(1)

# 전월의 수정 주가, 전년도의 수정 주가 컬럼 생성

month_last_df['BF-1M'] = month_last_df.shift(1)['Adj Close'].fillna(0)

month_last_df['BF-12M'] = month_last_df.shift(12)['Adj Close'].fillna(0)

month_last_df.head()

거래 내역 추가

# month_last = 구매 신호(momentum_index)를 확인하기 위함

for i in month_last_df.index:

signal = ''

# 절대 모멘텀의 계산식 → (전월의 수정 주가 / 전년의 수정 주가) - 1

momentum_index = (month_last_df.loc[i, 'BF-1M'] / month_last_df.loc[i, 'BF-12M']) - 1

# 0보다 크고 무한대가 아닌 경우가 구매 신호

flag = (momentum_index > 0) & (momentum_index != np.inf)

if flag:

signal = 'buy'

print(f'날짜: {i}, momentum_index: {momentum_index}, signal: {signal}')

df.loc[i:, 'trade'] = signal수익률, 누적 수익률 계산

# 수익률, 누적 수익률 계산

df['rtn'] = 1.0

# 수익률 계산

for i in df.index:

# 매수

if (df.shift().loc[i, 'trade'] == '') & (df.loc[i, 'trade'] == 'buy'):

buy = df.loc[i, 'Adj Close']

print(f"매수일: {i}, 매수가: {buy}")

elif (df.shift().loc[i, 'trade'] == 'buy') & (df.loc[i, 'trade'] == ''):

sell = df.loc[i, 'Adj Close']

rtn = sell / buy

df.loc[i, 'rtn'] = rtn

print(f"매도일: {i}, 매도가: {sell}, 수익률: {rtn}")

# 누적 수익률

df['acc_rtn'] = df['rtn'].cumprod()

# 최종 수익률

acc_rtn = df.iloc[-1, -1]

acc_rtn

번외: BuyandHold

# byandhold 수익률 계산

buy = df['Adj Close'].iloc[0]

sell = df['Adj Close'].iloc[-1]

print(sell/buy)

# 974.2744757914💻 함수화

1. STD-YM 생성 함수

def create_ym(_df, _col = 'Adj Close'):

df = _df.copy()

# Date가 column에 포함되어 있는가?

if 'Date' in df.columns:

df.set_index('Date', inplace = True)

df.index = pd.to_datetime(df.index)

df.index = df.index.tz_localize(None)

flag = df.isin([np.nan, np.inf, -np.inf]).any(axis=1)

df = df.loc[~flag, [_col]]

df['STD-YM'] = df.index.strftime('%Y-%m')

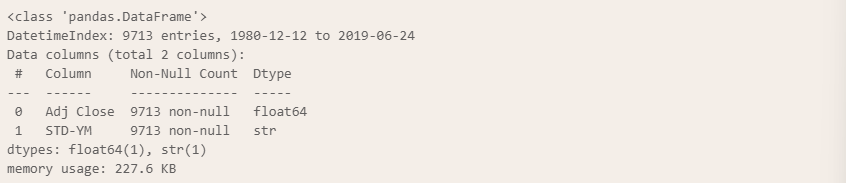

return dfdf = pd.read_csv('../csv/AAPL.csv')

ym_df = create_ym(df)

ym_df.info()

2. 월말 데이터 생성, BF1, BF2 column 생성 함수

def create_month(

_df,

_start = '2010-01-01',

_end = datetime.now(),

_momentum = 12,

_last = 1

):

if _last == 1:

df = _df.groupby('STD-YM').tail(1)

elif _last == 0:

df = _df.groupby('STD-YM').head(1)

else:

return "_last 값은 0 또는 1만 가능합니다."

col = _df.columns[0]

df['BF1'] = df.shift(1)[col].fillna(0)

df['BF2'] = df.shift(_momentum)[col].fillna(0)

df = df.loc[ _start : _end, ]

return dfmonth_df = create_month(ym_df)

month_df.head()

3. 거래 내역 추가, 수익률 계산 함수

def create_rtn(_df1, _df2, _score = 1):

df = _df1.copy()

df['trade'] = ''

df['rtn'] = 1.0

col = df.columns[0]

# _df2를 이용해서 거래 내역을 생성

for i in _df2.index:

signal = ''

# momentum 계산

momentum_index = _df2.loc[i, 'BF1'] / _df2.loc[i, 'BF2'] - _score

flag = (momentum_index > 0) & (momentum_index != np.inf)

if flag:

signal = 'buy'

# 거래 내역 생성

df.loc[i:, 'trade'] = signal

print(f'날짜: {i}, momentum_index: {momentum_index}, signal: {signal}')

# 수익률 계산

for i in df.index:

if (df.shift(1).loc[i, 'trade'] == '') & (df.loc[i, 'trade'] == 'buy'):

buy = df.loc[i, col]

print(f'매수일: {i}, 매수가: {buy}')

elif (df.shift(1).loc[i, 'trade'] == 'buy') & (df.loc[i, 'trade'] == ''):

sell = df.loc[i, col]

rtn = sell / buy

df.loc[i, 'rtn'] = rtn

print(f'매도일: {i}, 매도가: {sell}, 수익률: {rtn}')

# 누적 수익률 계산

df['acc_rtn'] = df['rtn'].cumprod()

acc_rtn = df.iloc[-1, -1]

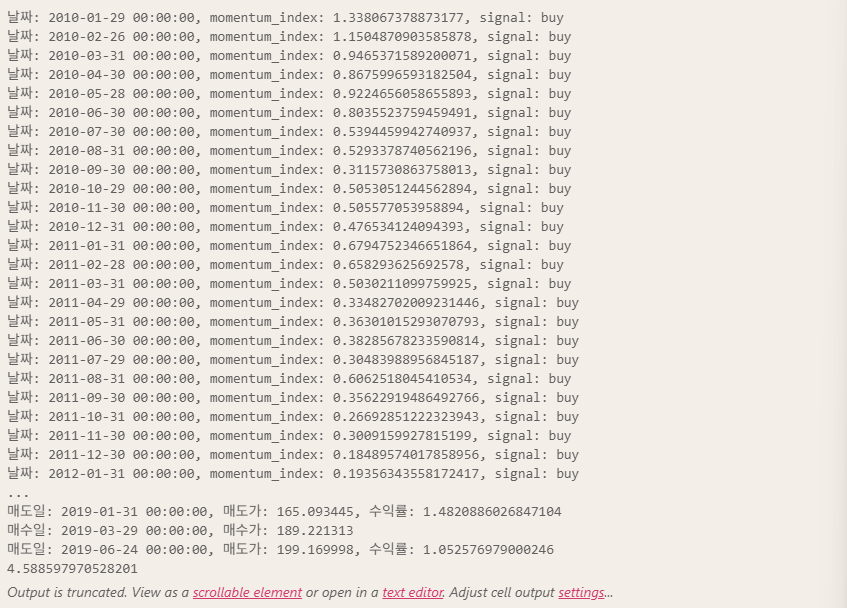

return df, acc_rtndf_final, acc_rtn = create_rtn(ym_df, month_df)

print(acc_rtn)

8주차 소감

다음 주 자연어 처리라서 쉬고 가는 타이밍을 만들어주셨는데 벌써부터 걱정된다...🥹

한글이 자연어 처리 중 가장 어렵다고 하는데... 물론 수업은 영어로 할 거지만 괜히 한글 자연어 처리에 대한 욕심이 생겼다고 할까?

원래 아무것도 모를 때 용감하다고 하지... 정신 바짝 차리자🔥

'멀티캠퍼스부트캠프' 카테고리의 다른 글

| 7주차 Note: 머신러닝/딥러닝 (0) | 2026.05.24 |

|---|---|

| 6주차 Note: 머신러닝 (0) | 2026.05.16 |

| 5주차 Note: 머신러닝 (1) | 2026.05.08 |

| 4주차 Note: 데이터 시각화 (0) | 2026.05.01 |

| 3주차 Note: 데이터 수집 (0) | 2026.04.26 |